28 April, 2026

What does China’s undisclosed strategic minerals catalogue reveal about its industrial priorities?

TT / Shutterstock

Summary

- An unreleased but seemingly authentic Chinese catalogue of 36 “strategic minerals” has surfaced in Chinese-language academic and policy-adjacent sources and is reportedly included in the five-year plan for mineral resources (2021–2025), despite neither the plan nor the list having been formally made public. Its reproduction in multiple independent sources strongly suggests it is genuine.

- China’s “strategic minerals” concept differs in important ways from Western criticality lists in scope, purpose, and selection logic. In China, “strategic minerals” are deemed essential for economic security, defence security, and the development of high‑tech industries, and are selected either because of supply vulnerability or because of China’s market dominance.

- The catalogue expands the previous list from 24 to 36 items with no removals, suggesting continuity in industrial priorities and refinement rather than methodological shift. Several additions relate to steelmaking and advanced military technologies, highlighting the enduring importance of infrastructure and defence capabilities.

- Classification within the strategic minerals framework has concrete policy effects, with different policy instruments applied – ranging from production targets or quotas and stockpiling to export controls and investment restrictions. Recent legal changes and central planning documents suggest that these linkages are being strengthened rather than diluted.

- The inclusion of additional raw materials where China dominates value chains and has restricted exports suggests strategic quality is increasingly tied not only to vulnerability but also to leverage, even as securing long-term domestic supply remains a foundational driver. This has direct implications for European supply security and industrial resilience, particularly through exposure to export controls.

In the last decade, global competition over the mineral raw materials required for low-carbon energy systems, digital communications, and advanced weapons systems has intensified. Many countries and jurisdictions, including the United States, the European Union (EU), Japan, and the United Kingdom, have developed lists of materials deemed “critical,” variously labelled “critical raw materials” or “critical minerals,” based on criticality assessments conducted by experts in government, academia, and industry.

The purpose of these lists is to identify materials of particular economic and strategic importance and to help guide policy attention and resource allocation. In the EU, their role has evolved from primarily raising awareness and informing research priorities to also supporting the identification of investment needs and measures such as recycling and, in some cases, new mining initiatives.

What are “critical” and “strategic” raw materials?

In the West, critical raw materials are typically defined along two main parameters: their importance to the economy and/or national defence, and supply risk – often stemming from dependence on one or a few suppliers.

While criticality lists typically focus on raw materials or elements, many of the most consequential bottlenecks in Western manufacturing lie not upstream at the mining stage, but downstream in advanced processing and the production of key components such as permanent magnets and batteries.

In some assessments, such as those carried out by the EU, “strategic raw materials” refers to a subcategory of critical raw materials, deemed essential for strategic objectives related to the “green transition” as well as defence and aerospace applications. More generally, whereas assessments of “critical” raw materials are primarily based on current and recent supply-demand trends, assessments of strategic raw materials place greater emphasis on anticipated future demand. As a result, strategic raw materials tend to be subject to prioritized political and regulatory measures.

While there is generally a good understanding of how lists of critical raw materials are negotiated and constructed in democratic systems, far less is known about how such lists are produced in China and how they function within Chinese policymaking. This knowledge gap matters because Chinese classifications of “strategic” raw materials shape domestic policy instruments that can directly affect global supply chains and, by extension, European supply security for a wide range of critical materials.

What was already known about Chinese raw materials assessments?

Previous research has examined how Chinese experts and government planners evaluate the importance of different raw materials, and how these assessments informed China’s first official catalogue of 24 “strategic minerals” approved by the State Council (China’s cabinet) and incorporated into the national mineral resources five-year plan in 2016. The plan provides little insight into the methodology used to select these minerals, only offering a brief rationale for establishing the catalogue, citing three overarching objectives: protecting national economic security, defence security, and the development needs of strategic emerging industries.

In the Chinese context, the distinction between “critical” and “strategic” raw materials is structured differently than in most Western frameworks. The term “strategic minerals” (战略性矿产) functions as the overarching official category in China, rather than as a subset within a broader class of “critical” (关键) minerals. The latter term does appear in Chinese academic discussions, however, where it is often used to refer to a narrower subcategory of strategic minerals, particularly materials needed in the officially designated strategic emerging industries, covering sectors such as semiconductors, aerospace systems, electric vehicles, and clean-energy technologies.

This difference in terminology, combined with the lack of transparency regarding the official selection methodology, raises questions about whether direct comparisons between the Chinese and Western lists are conceptually and practically meaningful. While Chinese experts and official sources frequently present the catalogue of “strategic minerals” as equivalent to Western criticality lists, it may be analytically more accurate to describe the Chinese exercise as an assessment of raw material “strategic‑ness,” rather than as a conventional criticality assessment, to better capture differences in scope, intent, and construction.

In sum, Western and Chinese lists differ in important ways in both content and selection criteria, and while Western lists of critical raw materials are increasingly used to inform and support policy action, China’s catalogue of “strategic minerals” is more deeply embedded in state planning and directly linked to regulatory and industrial policy instruments.

Fortunately, although the official methodology remains unavailable, there is a rich Chinese academic literature on “strategic minerals” that – together with the brief explanation provided in the mineral resources plan – allows some conclusions to be drawn.

What characterises Chinese assessments of “strategic minerals”?

One key characteristic of the Chinese concept and catalogue of “strategic minerals,” as identified in existing research, is its broader scope compared to Western approaches, both in terms of the materials included and the criteria applied. In Chinese assessments, raw materials may be considered “strategic” for three broad reasons: (1) they are essential to economic security, national defence, or strategic emerging industries – the three objectives explicitly stated in the plan; (2) they involve high supply risks due to domestic scarcity and import dependency; or (3) China holds a comparative advantage that provides it with market power and influence over global value chains.

This broader scope is evident in the Chinese catalogue, which covers multiple types of raw materials and distinct rationales for inclusion. It features several raw materials for which China faces supply security risks – many of them “bulk” or “staple” raw materials (大宗矿产) imported in very large volumes, such as iron ore and copper, as well as energy resources like oil and natural gas. Their inclusion highlights a well-known but often overlooked reality: despite its leadership role in many high-tech sectors, China retains many characteristics of a developing economy, with ongoing infrastructure expansion and resultant demand for bulk minerals and energy resources.

The catalogue also includes a second group of supply‑constrained raw materials that are imported in smaller volumes. For these materials, China typically imports ores or concentrates, processes and refines them domestically, and uses them in high‑tech industries. This group most closely resembles the critical raw materials identified in Western countries.

Finally, alongside import‑dependent materials, the 2016 list also features a subgroup of raw materials considered strategic primarily because of China’s domestic resource advantages rather than supply risk. Referred to as “advantageous strategic minerals” (优势战略性矿产), these materials provide China with leverage and influence over global markets. Rare earth elements (REE) are the most prominent example. Although supply risks may exist for some of these materials, Chinese academic discussions explicitly frame their strategic value mainly in terms of China’s resource advantages and resulting market power.

In recent years, information related to critical mineral resources and associated downstream technologies has become increasingly securitized in China, contributing to reduced transparency in planning and policymaking in this sector. In addition to the national five-year plan for mineral resources (2021–2025), several related plans have been withheld from public view, while access to government websites and other official resources has been restricted from outside China. The 2025 decision to stop publicly announcing REE mining and production quotas after more than three decades represents the latest example of a broader trend toward increasing secrecy.

What do Chinese sources reveal about China’s undisclosed 2021 strategic minerals catalogue?

Over the past two years, a Chinese list of 36 “strategic minerals,” reportedly included in the five-year plan for mineral resources adopted in 2021, has been discussed in Chinese-language academic articles, blog posts, commercial publications, and other non-official channels – despite neither the list nor the plan itself having been formally released to the public.

The existence and size of the 2021 catalogue was already noted in provincial-level administrative documents by at least mid‑2023. Identifiable descriptions of the 2021 catalogue and its 36 minerals can be traced as early as May 2024, when an academic article authored by researchers at the Chinese Academy of Sciences reproduced part of the list, explicitly naming 13 of the 36 minerals. In July 2024, a blog post presented the complete list, including all minerals mentioned in the academic article.

The scarcity of these early reproductions and their confinement to unofficial sources initially made it difficult to verify the list. This may help explain why the catalogue has not, to our knowledge, been systematically analysed in Western policy or academic work to date, despite occasional references in English‑language policy, technical, and institutional sources to the existence of an expanded but undisclosed Chinese strategic minerals catalogue.

However, since then – and especially from 2025 onward – a growing number of additional Chinese-language sources, including financial media and policy-oriented platforms, have independently referenced and reproduced the same list of 36 minerals. This convergence across source types and time strongly suggests that the catalogue circulating in Chinese-language public sources is an authentic reconstruction of the strategic minerals list embedded in China’s official mineral resources plan for 2021–2025.

What does the new catalogue tell us?

Although the lack of access to the full plan and the methodology underpinning the assessment limits the conclusions that can be drawn, the existence of a second, updated list of “strategic minerals” nonetheless enables comparisons over time. Such a comparison allows assessment of how China’s list has evolved and of its changing industrial priorities. Several noteworthy observations emerge from comparing the two lists.

- The list has expanded in line with global criticality trends

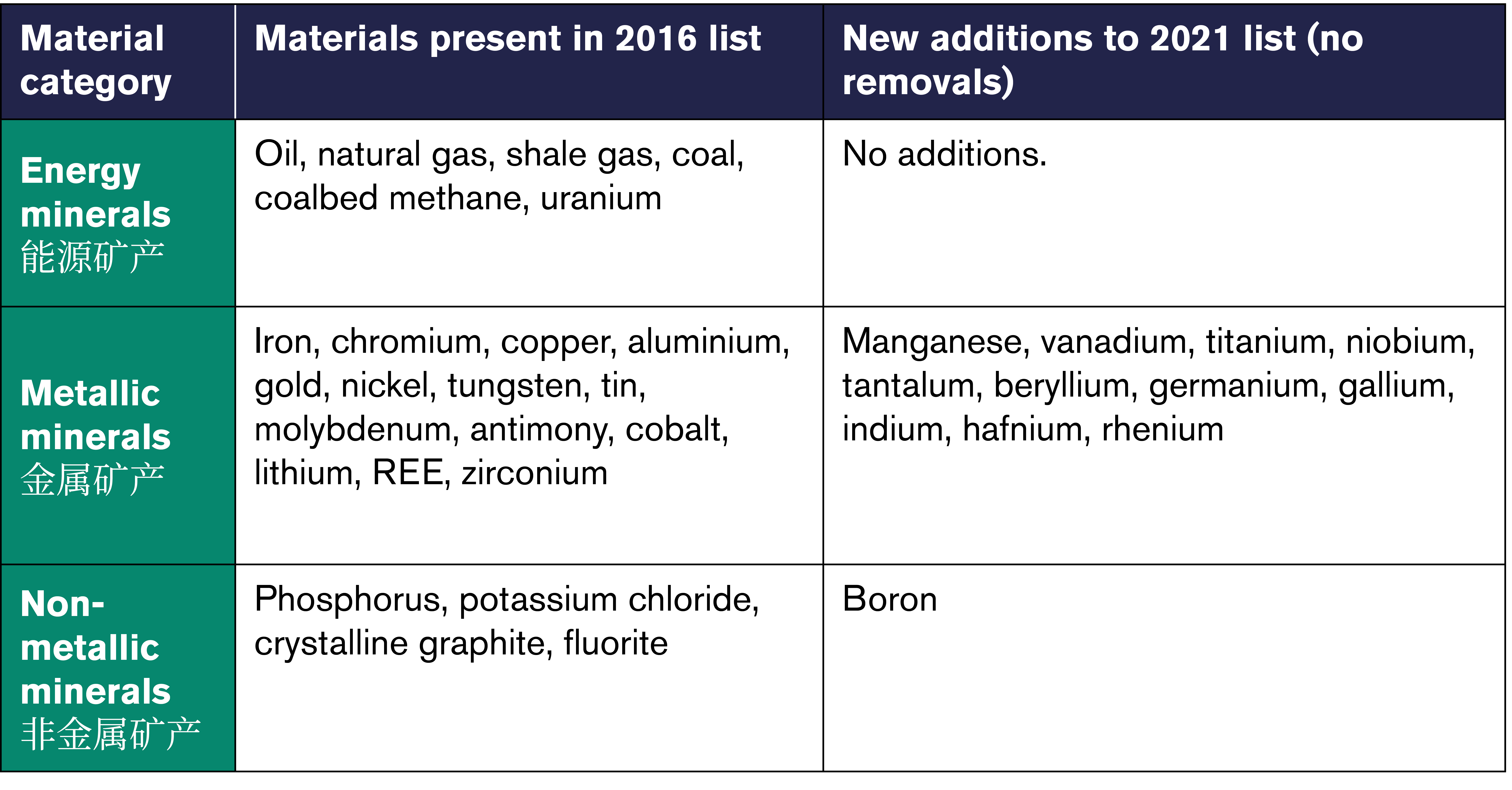

The most immediate observation is that the catalogue has expanded from 24 items in 2016 to 36 items in 2021 (Table 1). This mirrors a broader global trend toward longer lists of critical raw materials, reflecting both the growing complexity of modern technologies – which require a wider and more diverse range of inputs – and rising demand for these technologies. In the EU, for example, the list of has expanded with each revision, increasing from 14 items in 2011 to 34 in 2023.

Table 1. Expansion of China’s “strategic minerals” catalogue between 2016 and 2021

Source: Author’s own compilation, based on China’s National Plan for Mineral Resources (2016–2020) and Chinese-language policy-oriented sources reproducing the 2021 catalogue (including Dijinwang / 地产金融网 (2026)

- The list reflects continuity rather than a fundamental shift

Notably, none of the raw materials included in China’s 2016 catalogue were removed in the 2021 update. This stands out, as criticality assessments are inherently dynamic and updates to criticality lists typically involve the removal or replacement of some materials when others are deemed more critical. Instead, the 2021 update consists entirely of additions, with 12 new raw materials: boron, manganese, vanadium, titanium, niobium, tantalum, beryllium, germanium, gallium, indium, hafnium, and rhenium.

Core features of the 2016 list, including the broad categorization into energy, metallic, and non-metallic minerals; the inclusion of both supply‑constrained bulk minerals and small‑volume raw materials used in high‑tech industries; and the presence of so‑called “advantageous” raw materials – remain in place. This continuity suggests that the underlying methodology and rationales for inclusion have been refined rather than fundamentally revised.

- Continued focus on steel and military-industrial priorities

Of the newly added items, all but one (boron) are metallic minerals. While these metals have diverse applications, several are primarily used in steel alloys, including manganese, vanadium, and niobium. High-quality steel is a crucial dual-use input that supports both large-scale infrastructure development and military-industrial capabilities (see below).

Several of the newly added materials have clear defence and military-industrial relevance. Rhenium and hafnium are used in jet engines and gas turbines; vanadium, manganese and niobium in armour steels and high-strength alloys; and beryllium and hafnium in missile guidance systems, radar, satellites, and nuclear applications.

- “Strategic-ness” increasingly tied to China’s dominance

Building on the logic already present in the 2016 catalogue, the 2021 list adds several materials for which China holds a dominant position in global markets. This suggests that “strategic-ness” is increasingly defined not only by perceived vulnerability, but also by China’s ability to exercise market influence and regulatory power.

For example, germanium and gallium, both used in semiconductor production and both subject to Chinese export controls, have been added to the list. Their inclusion reflects their importance for semiconductor manufacturing and China’s position in key stages of their processing and regulation.

Indium, used in solar panels, LCD displays, and other consumer electronics, is another case in which China faces little upstream supply risk but instead derives strategic leverage from dominance in global processing. China introduced export licensing for indium in early 2025. Similarly, China faces limited upstream supply risk for hafnium, another material used in semiconductor production, as it is recovered from zirconium refining, a stage where Chinese companies dominate.

The growing prominence of such “advantageous” raw materials on China’s list aligns with broader trends in China’s global economic strategy: control over critical nodes in value chains is increasingly treated as a source of geopolitical leverage, even as securing long-term supply for domestic industries remains a central objective. While China’s policy actions have long been driven mainly by domestic objectives such as industrial upgrading and environmental protection, it has in recent years shown greater willingness to weaponize its value chain dominance externally. This shift is evident in tit-for-tat retaliatory measures taken in response to US export controls on semiconductors and related equipment.

China has long relied on quotas – and continues to do so, especially in the REE sector – alongside other domestic policy instruments to maintain control over supply chains, influence prices, and squeeze out foreign competitors. It has at times also resorted to informal export bans as a punitive tool to punish specific countries. These punitive measures were previously applied more sporadically and often undermined by fragmented governance and widespread circumvention.

In the past decade, however, the consolidation of critical mineral sectors, particularly the REE sector, has laid the groundwork for more effective weaponization. The Anti-Foreign Sanctions Law adopted in 2021, together with the Export Control Law adopted in 2020 (more extensively applied and expanded through implementing measures from 2023 onward), have provided the legal basis for this approach.

It is noteworthy that, despite China dominating the processing of most critical raw materials, it remains highly import-dependent for some of the newly added materials, particularly upstream ores and concentrates. This includes niobium, sourced primarily from Brazil and used in steel production, and tantalum, sourced largely from the Democratic Republic of the Congo and Rwanda and used in capacitors and other electronic components with dual‑use civilian and military applications, as well as in aerospace components.

The addition of boron is more ambiguous and highlights the difficulties of drawing firm conclusions about the drivers of “strategic-ness” for every material on the list. Boron is a key input for neodymium-iron-boron (NdFeB) magnets, which are powerful magnets used in electric vehicle motors. While China relies heavily on imports of boron concentrates from Turkey (the world’s dominant producer), these concentrates are predominately absorbed by non-strategic industries like glass, ceramics, and detergents.

From a value‑chain perspective, the most binding constraints for permanent‑magnet production tend to occur downstream rather than at the mining stage. In the case of NdFeB magnets, critical bottlenecks often arise on the REE side – particularly in the separation of individual elements and in alloy and magnet production.

A similar logic applies to boron. While some Chinese researchers have raised concerns about China’s high import dependence on upstream boron resources, the key vulnerabilities lie less in extraction than in downstream processing, in the production of high‑grade boron powder or highly purified ferroboron, where China holds a strong position within global value chains. It is therefore difficult to determine whether boron is considered “strategic” primarily because of supply risk, China’s ability to exercise downstream control, or a combination of both.

Why does China’s strategic minerals catalogue matter?

The classification of raw materials as “strategic” in China has direct policy consequences. Research shows that a range of policy instruments has been mobilized to support development of raw materials officially designated as “strategic,” and that different categories within this group may be subjected to distinct regulatory treatment (Table 2). This connection is reinforced in China’s newly released 15th Five‑Year Plan (2026–2030), which calls for further development of differentiated policies for exploration and extraction of strategic minerals.

Table 2. Classifications of strategic minerals and targeted policy measures

Note: Translated and adapted from Andersson, P. (2023), with revisions and additions by the author. Examples of classified minerals are illustrative and draw on a combination of official categorisations, academic discussions, observed policy implementation, and the author’s own interpretation.

Source: Andersson, P. (2020); China’s National Plan for Mineral Resources (2016–2020); Mineral Resources Law of the PRC (2024); China’s 15th Five-Year Plan (2026–2030).

Given the continued centrality of state planning in the Chinese economy, official strategic mineral lists are likely to have more far-reaching and concrete effects than in Western countries. In Europe and other market-oriented economies, critical raw materials initiatives – despite renewed emphasis on industrial policy over the past decade – often remain hampered by limited, fragmented, and inconsistent state support.

China’s strategic minerals catalogue is set to play an even greater role in mineral resources planning in the years ahead. In 2024, China’s Mineral Resources Law was revised to codify the State Council’s responsibility for establishing and revising the catalogue of “strategic minerals” as well as for determining measures related to exploration, mining, and stockpiling of materials on the list. A new catalogue is expected to be included in the forthcoming mineral resources plan for 2026–2030, although, as with the previous plan, it is not expected to be made publicly available. Official sources have already signalled, however, that high-purity quartz, used in strategic industries like semiconductors and solar panels, is slated for inclusion in the updated catalogue.

For European policymakers in particular, understanding how China defines “strategic” raw materials, and how these classifications trigger distinct, concrete policy instruments ranging from stockpiling and industrial support to export controls and investment restrictions, is therefore essential. China’s dominant position across many critical raw material value chains means that its domestic policy choices have global repercussions. This urgency is further heightened by the fact that China’s mineral strategy increasingly extends beyond supply security, aiming to preserve and strengthen value chain dominance in ways that can be weaponized.

Acknowledgements

This brief was produced as part of the NordForsk project 217380 Sustainable development of the Arctic Critical minerals in the Arctic: Challenges and perspectives for the Nordic countries (CRIMINA) led by the Fridtjof Nansen Institute.

The author is grateful to Per Kalvig, emeritus at the Geological Survey of Denmark and Greenland (GEUS), for valuable comments on a draft of this text.

{kind=link}

Technology as leverage: The rationale behind China’s export controls